How Long Does SR22 Last in Indiana? (Clock Starts Here — 3-Year Rule)

Last updated:

Indiana SR22 lasts 3 years for most violations — including driving without insurance, a first OWI/DUI, and reckless driving. It lasts 5 years for repeat OWI offenses or Habitual Traffic Violator (HTV) status. The SR22 stays on your Indiana driving record until the BMV officially releases you — not simply when you cancel the policy. The Indiana SR22 requirements set by the BMV determine exactly how long you are obligated to maintain continuous coverage.

If you are an Indiana driver dealing with a suspended license, understanding exactly how long your SR22 requirement lasts — and the precise steps to remove it without triggering a penalty — is the most important thing you can do to protect your wallet and your driving privileges. One missed payment resets the entire clock back to day one.

This 2026 guide covers everything Indiana drivers need to know: how to calculate your exact BMV end date, which actions will reset your clock, and the step-by-step process to safely remove the SR22 so you can transition back to standard, lower-cost auto insurance.

Quick Answer

You have to carry SR22 insurance in Indiana for 3 years for most violations, or 5 years for repeat OWI/DUI offenses and Habitual Traffic Violator (HTV) status. The requirement runs continuously from your official BMV reinstatement date — any lapse in coverage restarts the full period from day one.

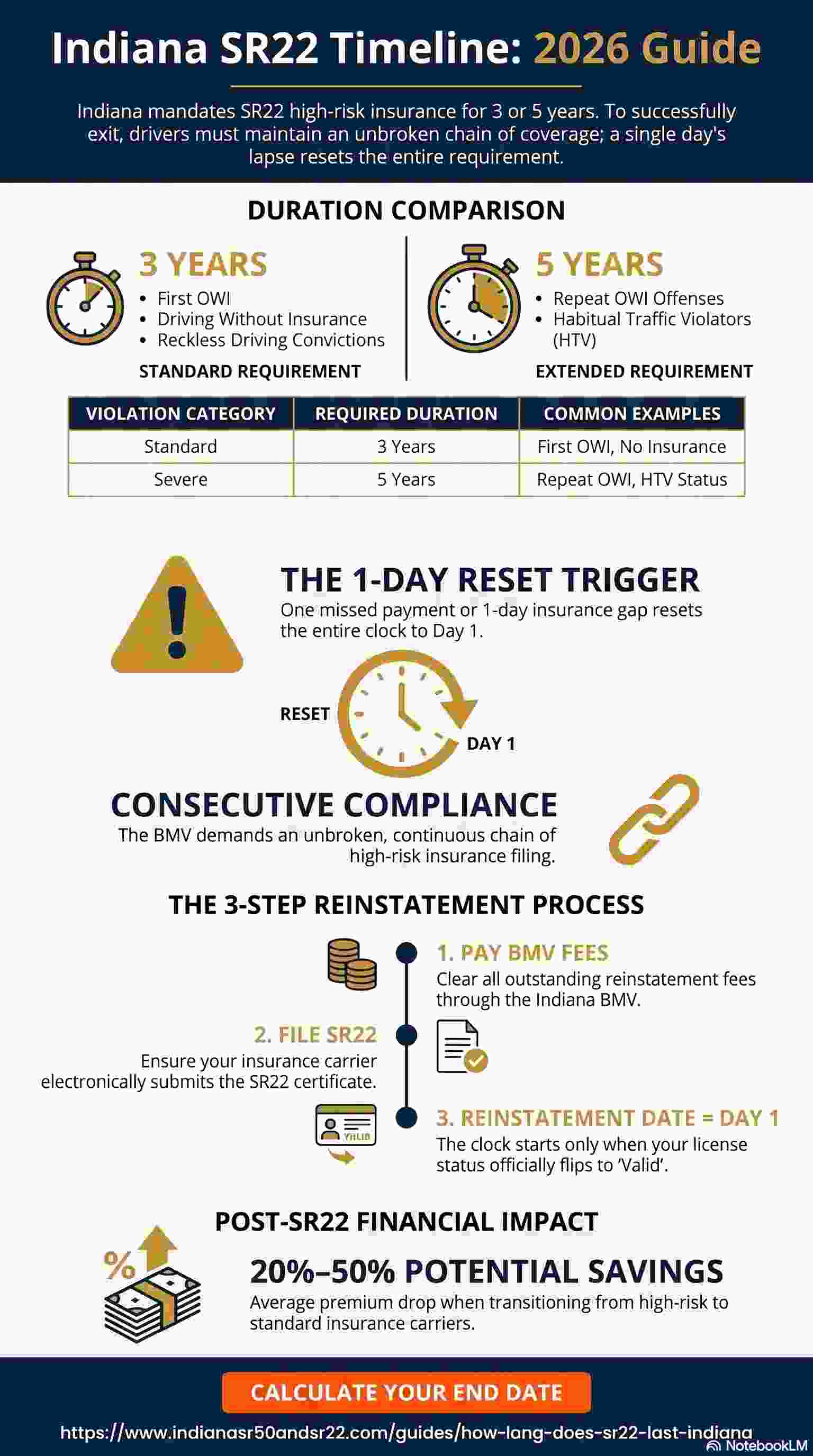

Indiana SR22 Timeline: This infographic shows how long SR22 lasts in Indiana

Click to expand +Indiana SR22 Duration Requirements: 3 Years vs 5 Years

The length of time you are required to maintain an SR22 certificate on file with the state depends entirely on the severity of the violation that led to your license suspension. Indiana categorizes driving offenses to determine whether you face a standard or extended probationary period.

Here is a breakdown of the SR22 durations by violation type in Indiana:

| Violation Type | SR22 Duration | Months | Indiana Code | Notes |

|---|---|---|---|---|

| Driving Without Insurance | 3 years | 36 | IC 9-30-6-12(b) | Standard penalty for failing to provide proof of financial responsibility. |

| OWI / DUI (First Offense) | 3 years | 36 | IC 9-30-6-12(b) | Standard duration for a first-time Operating While Intoxicated offense. |

| OWI / DUI (Repeat Offense) | 5 years | 60 | IC 9-30-6-12 | Extended duration for multiple severe infractions. |

| Reckless Driving | 3 years | 36 | IC 9-30-6-12(b) | Generally falls under the standard consecutive timeframe. |

| HTV Reinstatement | 3–5 years | 36–60 | IC 9-30-10 | Habitual Traffic Violator duration depends on the specific level and court orders. |

IC 9-30-6-12(b) governs the standard 3-year proof-of-financial-responsibility period for suspensions under IC 9-30-5, 9-30-6, and 9-30-9. The exact statutory trigger for the 5-year extension varies by specific circumstance and court order — always confirm your individual duration directly with the Indiana BMV.

When drivers ask how long does SR22 insurance last, the answer falls into one of two buckets: the standard three-year requirement or the extended five-year requirement.

Standard 3-Year SR22 Requirement

For the vast majority of Indiana drivers, the standard SR22 requirement lasts for three consecutive years. This period applies to drivers who have committed offenses such as driving without insurance, accumulating too many points on their driving record, or receiving their first OWI (Operating While Intoxicated) or DUI charge. Drivers convicted of SR22 insurance after an OWI in Indiana should pay close attention to exactly when their BMV reinstatement date is recorded, as even a short delay in completing all reinstatement steps will push back the start of the three-year clock.

The keyword here is consecutive. The Indiana BMV demands a continuous, unbroken chain of high-risk insurance coverage for 36 months. If your insurance policy cancels, expires, or lapses for even a single day during this three-year window, your insurance company is legally obligated to file an SR-26 form with the Indiana BMV. The SR-26 form notifies the state that your coverage has ended. Once the BMV receives this form, your license is immediately re-suspended, and your three-year clock is completely reset. This means that if you are two years and eleven months into your requirement and you miss a payment, you will have to start the three years all over again.

Extended 5-Year SR22 for Severe Violations

For drivers convicted of severe or repeat offenses, Indiana imposes a harsher penalty. If you have multiple OWIs, severe reckless driving incidents involving bodily harm, or if you have been classified as a Habitual Traffic Violator (HTV), you are typically looking at a five-year continuous SR22 requirement.

The Habitual Traffic Violator designation in Indiana is particularly strict. It is applied to drivers who have accumulated a specific number of major or minor traffic offenses within a 10-year period. Reinstating a license from an HTV suspension usually requires court intervention, specialized probationary licenses, and the extended five-year SR22 filing. As with the three-year requirement, this five-year period must be absolutely continuous. A lapse in month 59 will result in a reset back to month one, potentially trapping a driver in high-risk insurance premiums for a decade.

When Does the Indiana SR22 Clock Start? (BMV Reinstatement Date)

This is the most misunderstood aspect of the entire high-risk insurance process. Many Indiana drivers miscalculate their SR22 end date because they start counting from the wrong day.

Why "From the Violation Date" Is Wrong

A common assumption is that the SR22 clock begins on the day you were pulled over and issued a citation. This is completely incorrect.

The legal system moves slowly. If you are arrested for an OWI in January, you might not be convicted until April. The Indiana BMV's official long-term suspension and SR22 requirement are triggered by the conviction, not the arrest. Starting your countdown from the night you were pulled over will result in you canceling your SR22 policy months before you are legally allowed to do so, leading to an immediate license suspension. If you are navigating SR22 with a suspended license in Indiana, the gap between your violation date and your official BMV reinstatement date is often several months — every one of those months counts against you if you miscalculate.

Why "From the Filing Date" Is Also Wrong

Another very common misconception is that the clock starts the moment you purchase an SR22 policy and your insurance company files the certificate with the state.

While securing the SR22 is a crucial step, it is only one part of the reinstatement process. Let's say you buy your SR22 policy on June 1st. However, you still owe the Indiana BMV a $300 reinstatement fee, and you haven't yet submitted your court clearance documents. Your insurance company filed the SR22 on June 1st, but your license is still officially suspended. The BMV will not begin counting your three consecutive years just because you are paying for the insurance. If you wait three years from June 1st to cancel your policy, you will find out the hard way that your clock never actually started.

The Correct Answer: BMV Reinstatement Date Confirmed by myBMV

The definitive answer is the date your driver's license is officially reinstated by the Indiana BMV.

For the three-year or five-year clock to begin, three things must happen simultaneously:

- Your mandatory suspension period (ordered by the court or BMV) must be fully served.

- Your insurance company must have filed an active SR22 certificate with the Indiana BMV.

- You must have paid all necessary reinstatement fees to the BMV. If cost is a barrier, check whether you qualify for an Indiana license reinstatement fee waiver, which can reduce or eliminate the upfront cost of getting your license back.

Only when all three conditions are met will the Indiana BMV flip your license status from "Suspended" to "Valid" or "Reinstated." The date that status flips is Day 1 of your SR22 requirement.

For example: If you were arrested in January, convicted in March, bought SR22 insurance in May, but didn't pay your BMV reinstatement fees until August 15th — your three-year SR22 clock officially starts on August 15th.

What Resets Your Indiana SR22 Clock? (Common Mistakes That Cost You Years)

The Indiana BMV demands continuous proof of financial responsibility. Indiana does not grant grace periods for financial hardship or administrative errors. If your coverage drops, the clock restarts. Period.

If your coverage lapses at any point, your insurer will file an SR26 with the Indiana BMV, immediately suspending your license and pausing your compliance clock.

Here are the most common ways Indiana drivers accidentally reset their SR22 timeline.

Missing a Single Payment — How a 1-Day Gap Restarts Your 3 Years

Auto insurance companies are legally bound by Indiana state law to monitor SR22 policies tightly. If you miss your monthly premium payment, the insurer will typically issue a brief grace period (often 10 to 15 days, depending on the carrier). However, if that grace period expires and the payment is not received, the policy cancels at 12:01 AM on the cancellation date.

The exact moment your policy cancels, the insurance company's automated systems generate an SR-26 form. It is transmitted electronically to the Indiana BMV. Once the BMV receives it, your license is suspended immediately and your three-year compliance clock is wiped out. Even if you pay your bill the very next afternoon and the insurer reinstates your policy, you have technically had a lapse. You will now owe the state another full three years of SR22 from the date your policy is reactivated.

Switching Insurers Without Overlap — The Dangerous Gap

Many Indiana drivers realize they are overpaying for high-risk insurance and decide to shop for better rates. This is a smart financial move, but executing it poorly will ruin your progress.

If you find a cheaper rate with Insurance Company B, you might be tempted to cancel Company A today and start Company B tomorrow. Do not do this.

That one-day gap will trigger an SR-26 filing from Company A. The Indiana BMV will suspend your license and your clock will reset. To the state, any gap — even a few hours — is considered a failure to maintain continuous financial responsibility.

Getting a New Qualifying Violation During the SR22 Period

If you are currently serving a three-year SR22 term and you are convicted of another serious moving violation — such as another OWI, driving on a suspended license, or reckless driving — your current SR22 timeline will be discarded. The Indiana BMV will issue a new suspension, and once you become eligible for reinstatement again, you will be hit with a brand new, and likely longer, SR22 requirement. A second OWI during an active SR22 period will almost certainly elevate you to a five-year requirement.

How to Switch Carriers Safely Without Losing Time

If you want to save money by switching insurance carriers without resetting your Indiana SR22 clock, you must ensure an overlap in coverage. Here is the safest way to do it:

- Purchase the New Policy First: Secure your new auto insurance policy with the new carrier. Tell them explicitly you need an SR22 filing for Indiana.

- Set the Effective Date: Have the new policy begin immediately (e.g., today).

- Wait for State Acceptance: Allow 48 to 72 hours for the new insurer to electronically file your new SR22 certificate with the Indiana BMV and for the BMV to process it.

- Verify with the BMV: Log into your myBMV account or call the BMV to ensure the new SR22 is showing as active on your driving record.

- Cancel the Old Policy: Only after confirming the new SR22 is active with the state should you cancel the original policy.

By overlapping the policies by a few days, you guarantee there is no gap in coverage. The Indiana BMV will simply see that you transitioned from one valid SR22 to another, and your continuous three-year clock will remain perfectly intact.

How to Find Your Indiana SR22 End Date (3 Methods via myBMV)

Because the penalty for canceling your SR22 too early is so severe, you should never guess your end date. Always verify it through official Indiana BMV channels.

Here are the three methods to find your exact, legally binding SR22 release date in Indiana.

Method 1 — Check Your myBMV Online Account

The easiest and most accurate way to check your Indiana SR22 status is through the state's official digital portal.

- Go to the official Indiana BMV website and log into your myBMV account.

- Navigate to your "Driver Record" or "Reinstatement Requirements" section.

- Look for the SR22 compliance section. The system will clearly state whether your SR22 is currently "Required" or "Released."

- View your official reinstatement date. Add exactly three years (or five years for severe violations) to calculate the exact day your requirement drops off.

Method 2 — Call the Indiana BMV (888-692-6841)

If the online portal is confusing, or if you have a complex driving history with multiple suspensions, speak directly to a BMV representative.

Call the Indiana BMV Customer Service Center at 888-692-6841.

Ask them: "Can you please tell me the exact date my SR22 requirement expires and I am no longer required to carry it?"

Write down the date they give you, the name of the representative, and the time of your call. The Indiana BMV is the ultimate authority on your driving record.

Method 3 — Ask Your Insurer for the Termination Date on File

You can call your insurance agent and ask what date they have on file for your SR22 requirement to end.

Critical warning: Insurance companies are not the Indiana BMV. An insurer's internal systems might base your end date on the day you purchased the policy, not the day your license was reinstated. Always use your insurance agent's answer as secondary confirmation only — rely primarily on the Indiana BMV's official record.

How to Remove SR22 in Indiana: Step-by-Step BMV Process

Many Indiana drivers mistakenly believe that once they hit their three-year anniversary, the SR22 magically falls off their policy and premiums automatically drop. This is a myth.

Your insurance company will continue charging you for the SR22 filing and classifying you as a high-risk driver indefinitely until you take action. Here is the exact process.

Step 1 — Verify 3 Years Is Complete via myBMV Before Doing Anything

Do not make a move until you have absolute confirmation. Log into myBMV or call the Indiana BMV to ensure you have reached the exact date of your 3-year or 5-year requirement. If your official end date is October 15th, wait until October 16th to begin this process. Acting on October 14th could result in a devastating reset.

Step 2 — Do NOT Cancel Your Policy Before Confirming "Released" Status

Do not cancel your policy until your myBMV account explicitly shows SR22 status as "No Longer Required" or "Released." Canceling before this point will trigger an SR-26 form and result in an immediate suspension.

Step 3 — Contact Your Insurer to Remove the SR22 Rider

Once you have verified your release with the Indiana BMV, call your current auto insurance provider. Ask the agent to "remove the SR22 filing rider" from your policy. The insurer will verify this with the BMV system and stop filing the certificate on your behalf. Removing this rider typically results in an immediate small drop in your premium (the filing fee, usually $15 to $50). However, your base rate may still be high because you remain classified in a high-risk tier.

Step 4 — Immediately Shop for Standard (Lower) Rates

This is where you finally get your financial reward. Once the SR22 requirement is officially removed by the Indiana BMV, you are legally allowed to purchase standard auto insurance again. Your current insurer may not automatically transition you to their best preferred rate tiers.

This is the exact moment to gather quotes from multiple standard auto insurance carriers. Because you no longer require an SR22 filing, a large pool of standard and preferred insurers — who previously would have declined you — will now compete for your business. To find the most affordable coverage right away, compare options from the best SR22 insurance companies in Indiana and look at what they offer for standard policies once your filing obligation is lifted. Indiana drivers who complete their SR22 period and shop for new standard insurance typically see premiums drop 20% to 50%.

Step 5 — Confirm SR22 Is Marked "Released" on myBMV

As a final protective measure, a few weeks after you transition to standard insurance, check your myBMV account one last time. Ensure your license remains "Valid" and that there are no pending suspension notices. Filing errors happen — catching an administrative mistake early is far easier than fighting a wrongful suspension months down the road.

What Happens to Your Insurance Rates After Indiana SR22 Ends?

Dropping the SR22 is a major milestone, but Indiana drivers are often confused about exactly how it impacts their monthly bills.

How Much Do Rates Drop When SR22 Is Removed?

The moment the SR22 rider is removed, you save the monthly filing fee. But the real savings come from transitioning from a "non-standard" (high-risk) policy to a "standard" or "preferred" policy. Indiana drivers who complete their SR22 period and actively shop for new coverage typically see premiums drop 20% to 50%. The exact amount depends on your age, location, vehicle type, and the severity of the original violation. If cost has been a concern throughout your SR22 period, reviewing the cheapest SR22 insurance in Indiana options can also help you minimize premiums during the months remaining on your requirement before you transition to standard coverage.

How Long Does the Underlying Violation Stay on Your Indiana Driving Record?

It is vital to distinguish between the SR22 requirement and the underlying traffic violation.

In Indiana, your SR22 requirement might only last 3 years. However, the actual violation (e.g., a DUI/OWI, reckless driving) will stay on your motor vehicle record for much longer.

- Points from minor traffic violations in Indiana generally stay active on your record for two years.

- Major convictions, such as an OWI, can remain on your driving record for life, and insurance companies typically look back at the past 3 to 5 years of your driving history (and sometimes up to 7 to 10 years for severe infractions) when determining your rates.

Therefore, while you are no longer legally required to carry the SR22 form, an insurance company can still see the OWI from three years ago. Your rates will drop significantly because you don't need the SR22 filing, but they will continue to decrease year over year as the original violation ages further into the past.

The Best Time to Start Shopping for New Indiana SR22 Rates

If you are within 30 to 60 days of your Indiana SR22 expiration date, now is the time to start shopping. Note that if you do not own a vehicle, you are still required to maintain continuous coverage — a non-owner SR22 insurance Indiana policy covers your obligation without requiring you to insure a specific car, and the same shopping-ahead strategy applies.

By getting quotes for a standard policy that begins on the exact day your SR22 ends, you lock in lower rates immediately without risking a gap in coverage. Comparing rates 30 days before your release date ensures you don't pay a single day more of high-risk premiums than legally necessary. You can also use the Indiana license reinstatement calculator to map out your exact timeline and confirm how many days remain before you can make the switch.

Indiana SR22 Duration — Frequently Asked Questions

Here are the most frequently asked questions from Indiana drivers about SR22 duration, expiration, and removal.

How long do you have to carry SR22 insurance in Indiana?

You have to carry SR22 insurance in Indiana for 3 years for most violations, including driving without insurance and a first OWI/DUI conviction. You have to carry it for 5 years for repeat OWI offenses or Habitual Traffic Violator (HTV) status. The requirement runs continuously from your official BMV reinstatement date, and any lapse in coverage restarts the full period from day one.

How long does SR22 stay on your record in Indiana?

The SR22 filing requirement stays on your Indiana driving record for 3 to 5 years depending on your violation. However, the underlying conviction (such as an OWI) may remain on your driving record far longer — major violations like DUI can appear for up to 10 years and affect insurance rates even after the SR22 requirement ends.

How do I find out when my Indiana SR22 expires?

Log into your myBMV account and check the Reinstatement Requirements section — it will show whether your SR22 is still "Required" or has been "Released." Alternatively, call the Indiana BMV at 888-692-6841 and ask for your exact SR22 release date. Add 3 years (or 5 for severe violations) to your official BMV reinstatement date to calculate your end date.

What is the SR22 grace period in Indiana?

Indiana does not grant a formal SR22 grace period. If your SR22 insurance payment is missed, your insurer will apply their own grace period (typically 10–15 days). If payment is not received before that grace period expires, the insurer files an SR-26 cancellation form with the Indiana BMV. Your license is immediately suspended and your 3-year SR22 clock resets to day one.

Does SR22 end automatically in Indiana, or do I need to do something?

It does not end automatically with your insurance company. While the Indiana BMV system will automatically note that the requirement has been fulfilled, your insurance company will continue to charge you for the SR22 filing and keep you on a high-risk policy until you explicitly contact them to remove it and renegotiate your rate.

Can I ask the Indiana BMV to end my SR22 early?

No. The SR22 duration is mandated by Indiana state law. Neither the BMV staff, a judge, nor your insurance agent has the authority to terminate your three-year or five-year continuous requirement early. You must complete the full duration.

What if my insurer cancels my policy before my 3 years are up?

If your insurer cancels your policy (whether due to non-payment, too many claims, or they are exiting the market), they will file an SR-26 form with the Indiana BMV. To prevent your clock from resetting, you must secure a new SR22 policy with a different carrier before the cancellation date of the old policy. If a gap occurs, you lose all your accumulated time and start over at day one.

Does the SR22 period reset if I get another violation in Indiana?

Yes. If you receive a new conviction that requires an SR22 while you are already serving an SR22 period, the Indiana BMV will issue a new suspension. Your timeline will reset based on the reinstatement date of the new violation, and the required duration may be extended from three years to five years depending on the severity.

Does my Indiana SR22 transfer if I move to another state?

Indiana's SR22 requirement is tied to your Indiana driving record. If you move to another state, that state's DMV will typically recognize the obligation and may require you to maintain a comparable SR22 filing in your new state. You cannot escape the requirement by moving — your new insurer will need to file an SR22 (or equivalent financial responsibility form) in both states during the transition. Contact the Indiana BMV at 888-692-6841 before moving to get exact guidance on your specific record.

Disclaimer: The information provided by Indiana SR50 and SR22 is intended for educational purposes only and reflects Indiana BMV regulations as of 2026. Auto insurance laws and state requirements are subject to change. Always verify your specific driving record, SR22 status, and legal requirements directly with the Indiana Bureau of Motor Vehicles or your licensed insurance provider.

Read More

What Is an SR26 in Indiana?

The SR26 cancellation form explained — what triggers it, what it does to your license, and how to fix it.

Indiana SR22 Requirements 2026

Everything you need to know about BMV SR22 requirements and reinstatement.

SR50 Insurance Guide 2026

Understand the Indiana SR50 form, when the BMV requires it, and how to get covered.

SR22 & SR50 Forms Explained

The difference between forms, how they are filed, and why you can't do it yourself.

Know the Requirements for Reinstatement Now

Takes 2 minutes. No commitment.

Reinstatement Calculator — Free →